Biodiversity and CSRD: From Complexity to Concrete Action

BLOG

Biodiversity is an increasingly urgent but complex topic — deeply intertwined with other environmental themes like climate, water, and pollution, but also with social themes, such as "affected communities." The loss of biodiversity is not an abstract, distant crisis: it is a real and escalating threat, one that could undermine economies and societies as we know them.

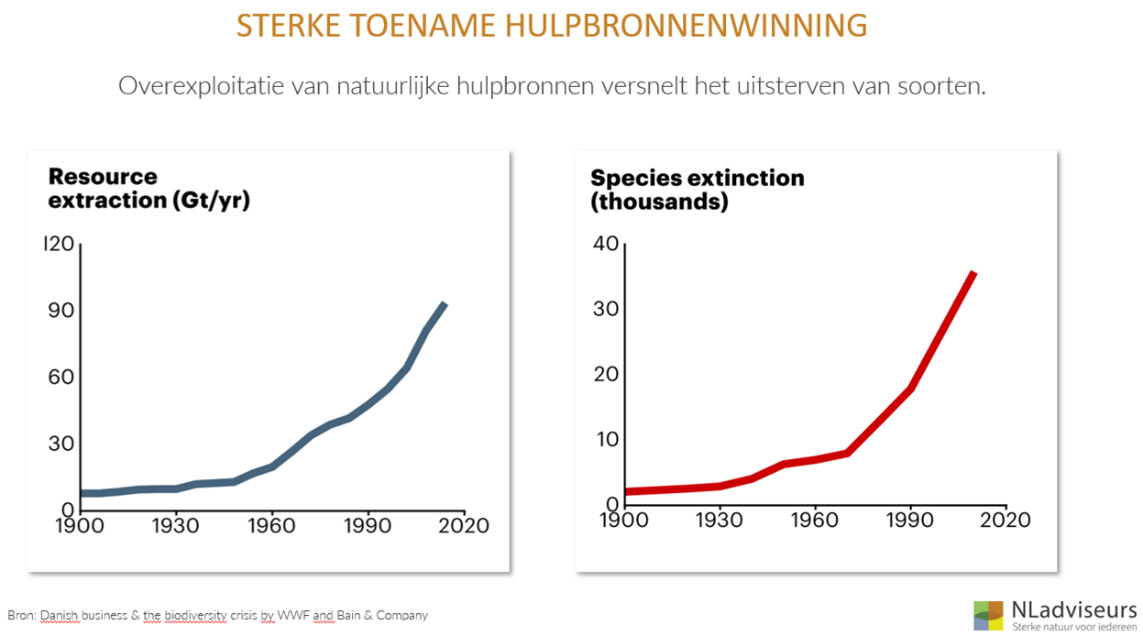

During our recent webinar with NLadviseurs on April 8, we tried to shed some light on the subject. Nature’s decline is accelerating at a rate that’s difficult to grasp — wild animal populations have plummeted worldwide by 69% since 1970. These human-driven extinction rates since the industrial revolution should be setting off alarm bells. In fact, in some ways, nature operates much like a supply chain, where the removal of key components leads to systemic collapse. And here’s the harsh truth: while nature will eventually recover, humanity may not.

The webinar underscored our dependence on nature’s “ecosystem services” — from fertile soil, clean water, and pollination to climate regulation and natural pest control. As these systems degrade, the economic consequences become unavoidable: scarcer resources, poorer air and water quality, endangered food security, and, ultimately, rising public costs for ecological restoration. In short, this isn’t just an environmental issue, it’s a financial one.

But what does this mean for businesses? As the conversation moved toward solutions, the focus shifted to action: reducing negative impacts across land, freshwater, and sea use; limiting pollution and resource extraction; curbing the introduction of invasive species; and actively improving biodiversity on company grounds. Some organizations are even beginning to map the species living on their sites, identify nature-related business opportunities, and develop transition plans aimed at turning negative footprints into net-positive contributions.

Following this broader perspective, we zoomed in on the practical side: biodiversity reporting under the Corporate Sustainability Reporting Directive (CSRD), specifically the E4 standard for biodiversity and ecosystems. Using real-world data from Dutch and European companies, we explored how organizations are approaching this new reporting landscape.

A few key takeaways:

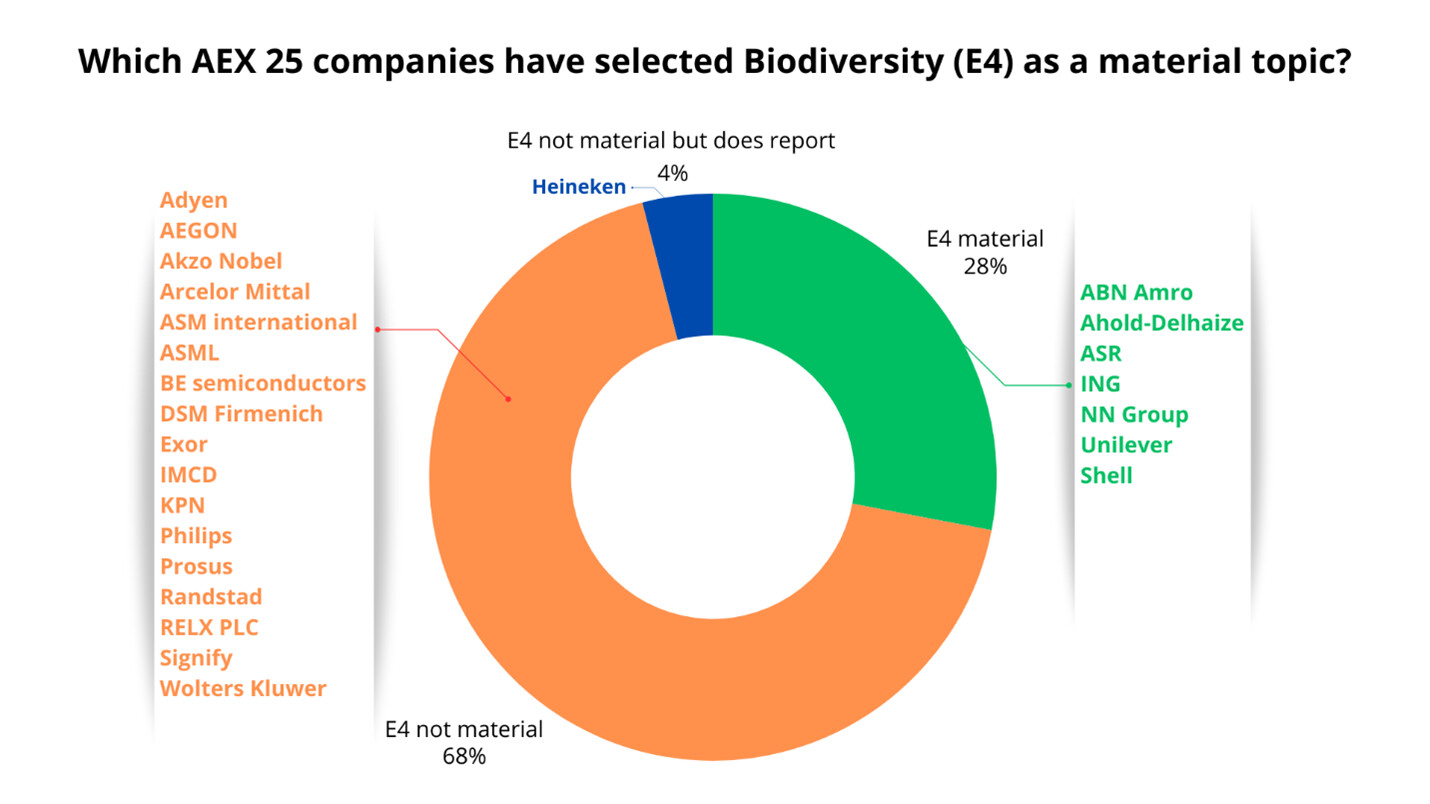

- A significant number of companies recognize biodiversity as a material theme — but the road from recognition to concrete action is still being built — strikingly, some food-related companies have not (yet) classified biodiversity as material.

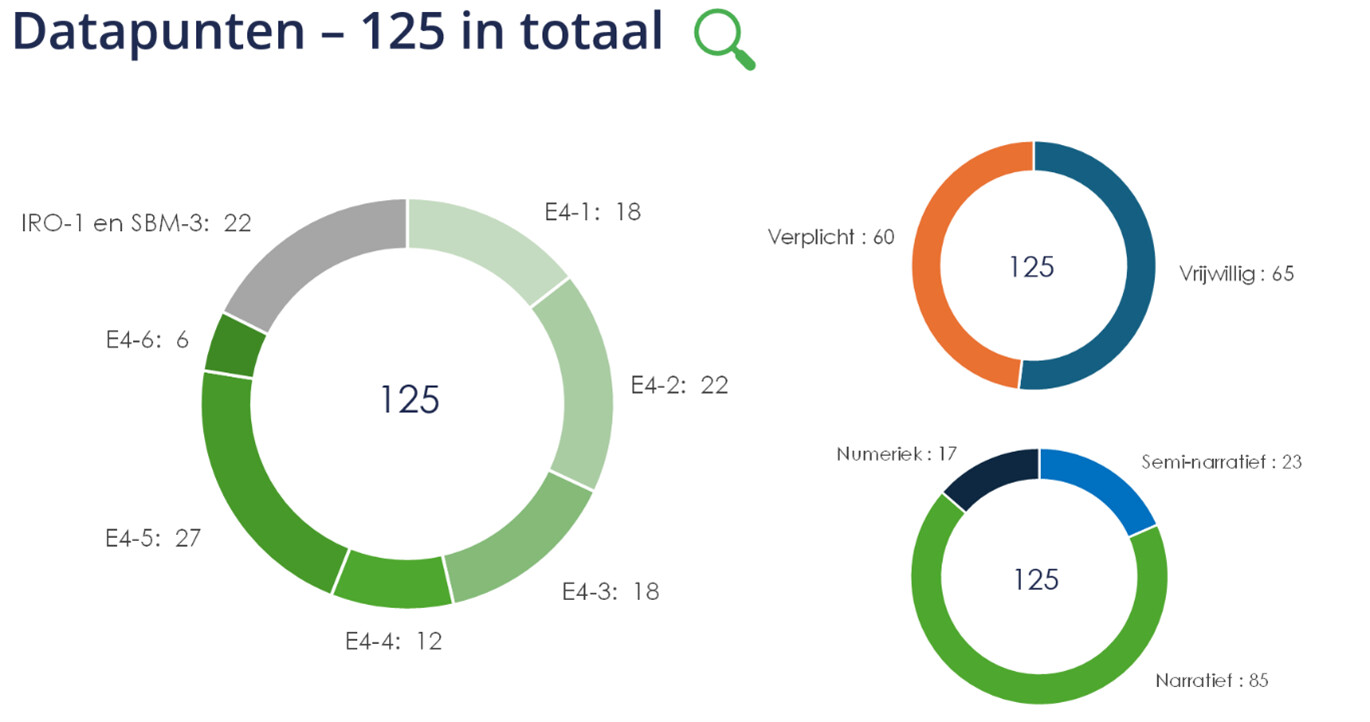

- Reporting under E4 involves 125 data points, with a clear split between mandatory and voluntary disclosures. The challenge lies in meaningful reporting, not just ticking boxes.

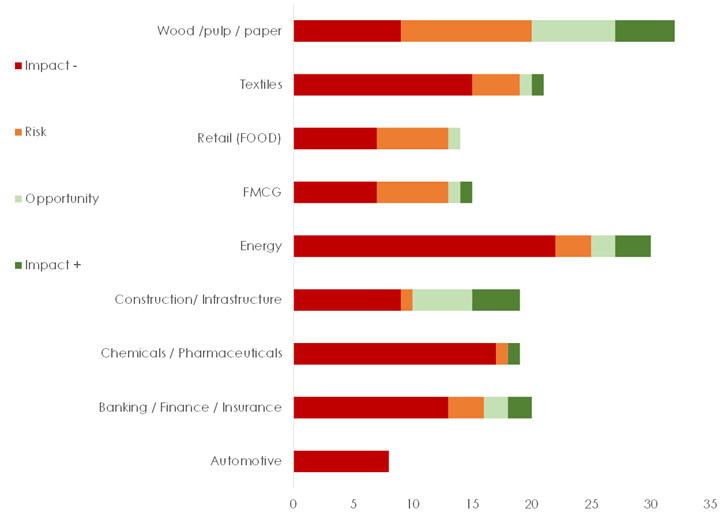

- Our analysis revealed an imbalance: companies are much more likely to report on risks than on opportunities. This suggests that there’s still untapped potential for biodiversity-driven business value.

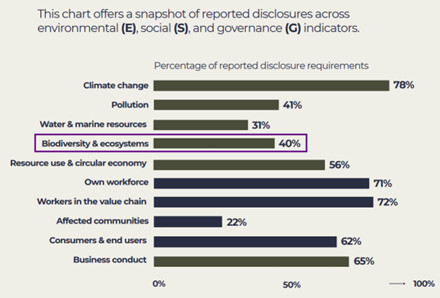

According to Copenhagen Changery, in the CSRD reports published so far since the beginning of 2025, only 40 % of the disclosure requirements related to Biodiversity were reported, which can be attributed to data availability, knowledge and experience in reporting on this subject. Many companies struggle to understand and measure the impact of their operations and supply chains on biodiversity. Graph source: linkedin.com/company/copenhagen-changery.

According to Copenhagen Changery, in the CSRD reports published so far since the beginning of 2025, only 40 % of the disclosure requirements related to Biodiversity were reported, which can be attributed to data availability, knowledge and experience in reporting on this subject. Many companies struggle to understand and measure the impact of their operations and supply chains on biodiversity. Graph source: linkedin.com/company/copenhagen-changery.

Our analysis of reported IROs in the 2024 CSRD reports released so far. The analysis covered a non-exhaustive selection of 31 Dutch and other European companies who had classified Biodiversity (E4) as a material theme.

We also shared hands-on tips for companies already thinking about their 2025 reports, such as:

- Avoid clustering multiple Impacts, Risks, and Opportunities (IROs) into a single generic description.

- Don’t skip the IRO narrative by simply referring to the sub-topic name.

- Pay close attention to the entire value chain — upstream and downstream — when identifying nature-related dependencies and risks. Ask persistently, where do the materials come from in the products we buy, and where do our products eventually end up?

On specific disclosure requirements, we noticed recurring themes:

- Under E4-2 (Policies), traceability is often the first step. Companies are increasingly focused on tracking materials like palm oil, soy, coffee, leather, wood, paper, cotton, metals, and mining products. Regenerative agriculture also appeared as a growing practice to reduce biodiversity loss linked to intensive agriculture.

- For E4-3 (Actions), many organizations are still struggling to make biodiversity measurable. Yet innovative solutions like AI-based biodiversity monitoring and partnerships with nature conservation experts are already being explored — often through pilot projects designed to test net-positive solutions.

- E4-6 (Financial Implications) remains a work in progress. This disclosure is subject to a phase-in period, meaning companies have some breathing room in the coming years – but nature's clock is ticking.

We wrapped up the session with a clear message: biodiversity reporting doesn’t have to be overwhelming, but it does require structured action. Our proposed “Roadmap for Biodiversity” helps organizations break down this complex theme into manageable steps, from impact analysis to setting ambitions and transition planning.

Curious how biodiversity can strengthen your organization on the path to sustainable value creation? Let’s continue the conversation — get in touch with us. We’d be happy to start with a no-obligation introductory meeting where we can discuss your needs and challenges and explore how you can make nature an integral part of your sustainability strategy.

Back to news