How to do a double materiality analysis that complies with CSRD

Blog

Double materiality analysis plays a key role in the requirements of the new European Corporate Sustainability Reporting Directive (CSRD). The analysis identifies the sustainability issues that are relevant (i.e. material) to your company, and therefore must be included in its annual report. It also provides focus. Future-proof companies will benefit from including these issues in their business strategy, as they mark where opportunities and risks lie, for the company and its stakeholders. Or for both of these groups – in which case shared value arises. Climate change provides an example. Organisations influence climate change, but are themselves also affected by climate change. For instance, by its effects in raising raw material prices, or increasing the risk of business premises being flooded. While a climate-focused intervention, such as mounting solar panels on business premises, can create shared value – that benefits both the business and the community.

What does double materiality mean?

Materiality analysis is a concept that has been known for years - for instance, as a component of voluntary reporting guidelines such as the GRI. The CSRD introduces the concept of double materiality analysis in order to clarify the impact of sustainability topics from two perspectives:

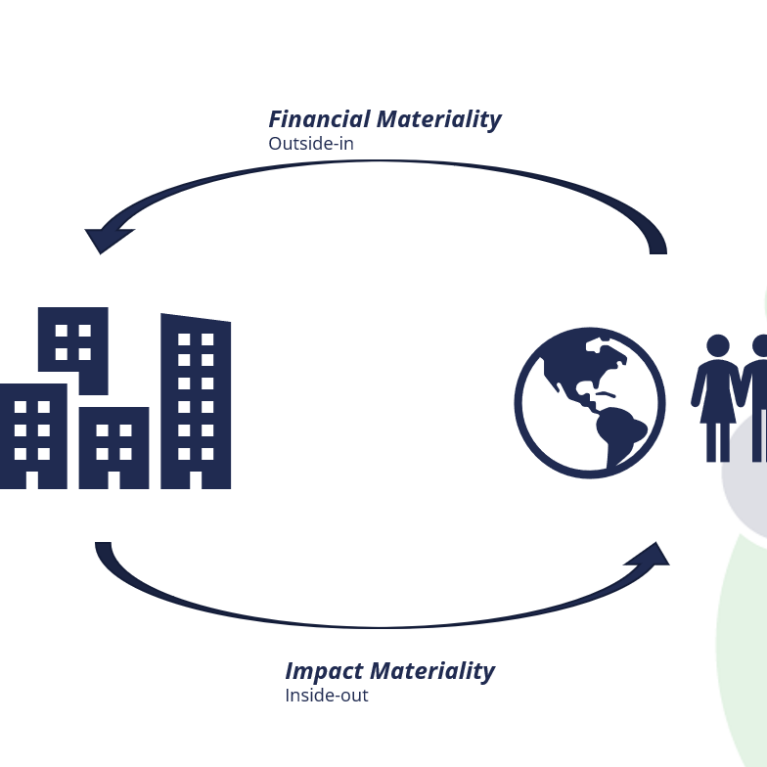

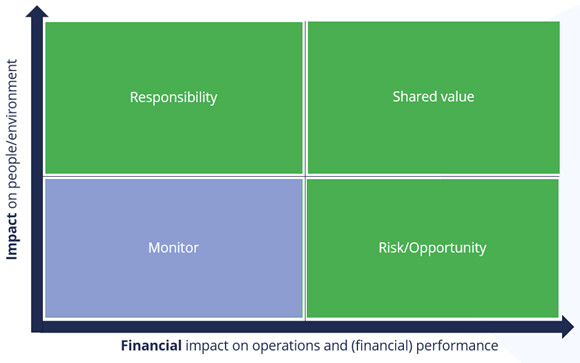

- An outside-in perspective, or financial materiality: What is the impact of a topic on the (financial) performance of the organisation? (See the x-axis in the figure below.)

- An inside-out perspective, or impact materiality: What is the organisation's impact on people and the environment? (See the y-axis in the figure below.)

If the answer to either of these two questions is 'MAJOR', the sustainability topic is material to your organisation. It falls into the green areas in the figure, below. The CSRD requires your organisation to report on this sustainability issue, and to include in the report its policies, actions, targets and KPIs.

How do you determine an issue’s impact?

Answering the above two questions on financial and impact materiality may seem simple, but is challenging in practice. A double materiality analysis must also comply with a number of requirements. Fortunately, the CSRD also provides guidance. To determine relevant sustainability issues, one looks at the actual, potential, positive, negative, direct and indirect effects of an issue, in the short, medium and long term, throughout the value chain. So even issues with an indirect impact, like a supplier’s poor working conditions, could be material. The mandatory due diligence procedure provides much information on (potential) negative impacts throughout the value chain. To determine the impact of an issue, the assessment criteria to be applied are: the severity of the impact (scale), and how widespread the impact is (scope). For potential impacts, probability also plays a role. And for a negative impact, recoverability is also relevant in assessing the relevance of a sustainability issue. The active involvement of stakeholders is central to establishing a materiality analysis. The process of materiality analysis must be described, according to the CSRD, and include logical threshold values for labelling an issue as material or non-material.

Roadmap for CSRD materiality analysis

After conducting many materiality analyses, we concluded that getting good information requires more than a simple questionnaire. The CSRD clarifies a process that also improves the comparability of the information gathered. TOSCA’s experience has allowed us to identify the steps set out below, to help you comply with CSRD requirements:

- Set up a working group consisting of the relevant people in your organisation

- Identify potential material issues, based on ESRS, SDGs, sector standards and reports, previous stakeholder consultation, etc. (long list)

- Assess the impact of each potential sustainability issue on your value chain, based on criteria such as severity, scope, likelihood and recoverability

- Select from the potential material issues those that are actually material to your organisation; working together with management and stakeholders

- Visualise the materiality analysis

- Monitor developments and adjust the materiality analysis where necessary

Make sure you properly document choices and trade-offs at each step, for the purpose of external verification (limited assurance).

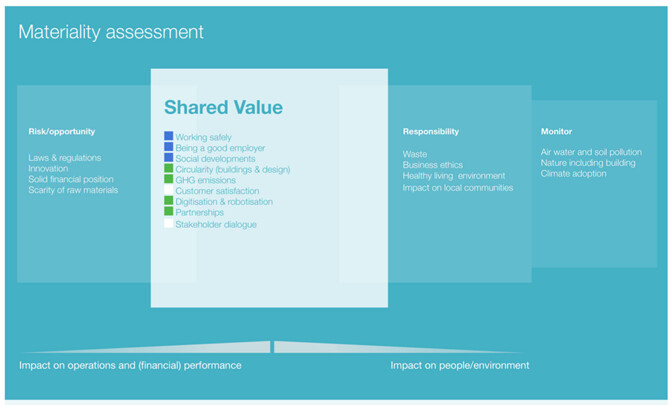

Example of a CSRD double materiality analysis

Few double materiality analyses have been published, but this will soon change. Last year, working with Daiwa House Modular Europe, we produced the double materiality analysis set out below. We recommend that the organisation’s annual report should also include an explanatory table, explaining the impact of each material issue. Also include page number references to the policies, actions and targets relevant to these issues.

What does a materiality analysis provide?

Producing a materiality analysis is an exciting, shared exercise that provides extensive and useful information on opportunities, risks and impacts, as well as input to the organisation’s strategy. As the objectives and projects are detailed for each issue, the potential benefits become increasingly visible. The positive impacts start to emerge. And the analysis process starts generating its own energy. This is when the CSRD becomes more than a reporting guideline. Its outcomes can be integrated into your existing management processes, which we recommend for the ongoing development of a successful and future-proof organisation.

Get more information on double materiality analysis - without obligation.

Let’s meet! Email christien@toscatribe.nl or call 0610 008 736.

Back to news