Is AI Your New ESG Manager...or an Overconfident Intern?

BLOG

A practical guide to where AI genuinely helps with ESG processes, and where it creates more risk than it removes.

The ESG technology market wants you to believe the future of sustainability reporting is simple: connect your systems, let the AI run, and your CSRD report writes itself. The vendors promise significant cost reductions, automated materiality assessments, and audit-ready outputs generated in days rather than months.

Some of that is real, and much of it is not. A lot is at stake when your management board is signing off on legally binding disclosures, and when the auditor arrives.

Over the past year, we've worked with companies navigating this question: where does AI genuinely help, and where does it create new risks? This article is our honest answer.

The promise vs. the audit reality

There's a seductive narrative right now: AI can automate the ESG compliance burden end-to-end. Feed in your data, get out a CSRD report. This framing misunderstands what CSRD actually requires, and what auditors are looking for.

Under CSRD (and also following Omnibus), limited assurance on sustainability data remains mandatory. Assurance is about whether every material statement can be traced back to a verified, consistent source, with a documented methodology and a named human accountable for it.

An AI-generated narrative, however fluent and well-structured, is not an audit trail. A materiality assessment produced by an algorithm, without documented human judgement at each decision point, is not defensible to a third-party assurer. As such, AI is transforming the compliance burden, rather than eliminating it: While it reduces the time spent on manual data gathering, it demands more attention to ensure accountability for outputs that look entirely credible on the surface, but may lack the correct processes and known, transparent assumptions underneath.

There's a subtler problem too: AI doesn't know what your data means. Every data point in an ESG report sits in a context that sustainability professionals understand intuitively; which entity it belongs to, which reporting period, how it was collected, how confident you are in it. AI has none of that background unless you explicitly provide it. If you feed it a spreadsheet of energy consumption figures without explaining the scope boundaries, the collection methodology, or the gaps, it will produce something that looks coherent and complete. That surface polish is precisely the danger. The cost of missing context isn't that AI stops working, it's that it keeps working, confidently, on assumptions you didn't know it was making.

Here's another uncomfortable reality: across ESG topics, from energy and emissions to social indicators and supply chain due diligence, data quality remains the biggest limiting factor. Sustainability data is typically fragmented across systems, collected at different frequencies, owned by different parts of the organization, and subject to varying degrees of verification. AI cannot fix what the underlying data doesn't have. Scope 3 emissions are the most visible example: nearly half of sustainability leaders lack confidence in the accuracy of their own figures, and no amount of AI processing turns incomplete supplier data into credible disclosure. The same logic applies to social metrics gathered through inconsistent HR systems, or environmental data reported by sites using different methodologies.

None of this means AI has no role. It has an enormous role — just a different one than software vendors typically describe.

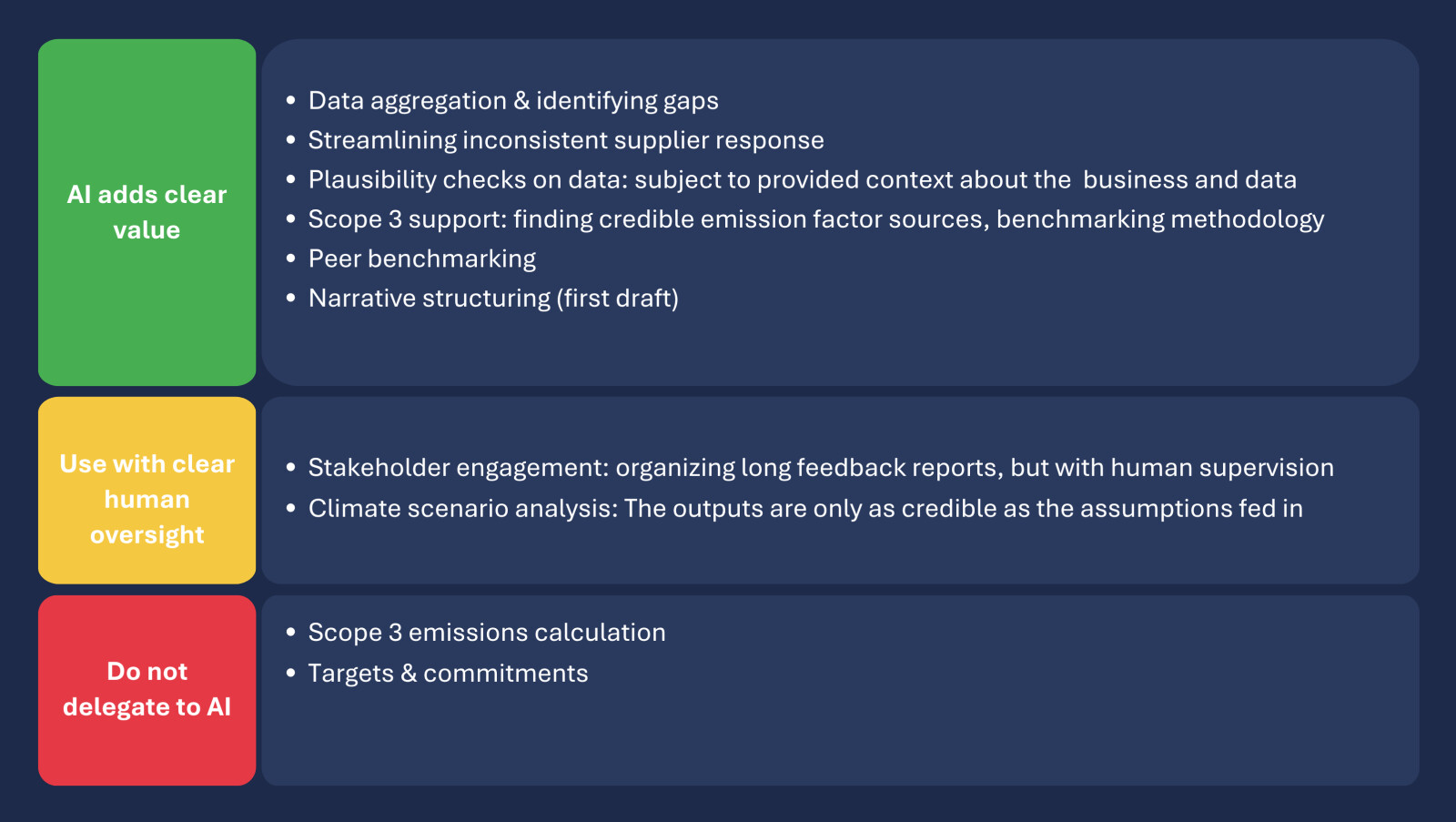

TOSCA's AI traffic light: what to delegate, what to assist, what to own

We use a three-tier framework to guide automation. See these below:

What responsible use actually requires

Frameworks like the traffic light above are useful for orientation. But in practice, the boundary between each tier shifts depending on your material ESG topics, data maturity, your reporting scope, and your assurance provider's expectations. What's safe to automate for a company with three years of audited ESG data and a dedicated reporting team looks very different for one preparing its first CSRD disclosure.

What we consistently see is that before asking AI for output, four questions need to be answered and clarified for it:

- What is the source of the data, and who owns it?

- What does the data represent?

- What do you not know or are uncertain about?

- Can you reconstruct every output for an auditor?

These are organisational questions, which we work through with clients before any AI-automation begins.

A useful reframe: think of AI not as an all-knowing prophet, but as a very capable intern joining your team as a fresh graduate. Bright, fast, technically proficient. But with no institutional knowledge, no feel for your organisation's specific context, and a strong tendency to produce polished-looking answers even when the underlying reasoning is shaky. You wouldn't hand a new graduate your raw data and ask them to produce a board-ready disclosure without briefing them thoroughly, checking their work, and pushing back on anything that looks too clean. The same discipline applies here. Define what AI can and cannot do in your process. Challenge outputs rather than accepting too quickly, and mistaking fluency for accuracy.

The companies that use AI most effectively in their ESG programs have first built the organizational foundations of their ESG management and assigned clear data ownership and cross-functional alignment between different departments. This is what we call ESG embedding, and it's the precondition for responsible AI adoption.

This is essential, as AI is a multiplier. If your ESG data and processes are fragmented, AI makes fragmented outputs faster. With solid foundations, AI enhances your ESG performance and helps you move faster towards your targets.

Looking to take the next step in using AI for ESG? Contact us: pedram@toscatribe.nl