Double Materiality Assessment – What’s next?

CSRD gap analysis

Many companies are actively conducting their Double Materiality Assessments. Have you completed yours? More importantly, do you know the steps to take afterward? Before we explore what comes next, let's briefly revisit the concept.

The Double Materiality Assessment

Introduced by the Corporate Sustainability Reporting Directive (CSRD), the Double Materiality Assessment aids companies in pinpointing key sustainability topics that are critical both within their operations and across their value chain. This assessment considers two distinct perspectives: the external "outside-in" perspective, which assesses financial materiality and its implications for the organization's financial performance, and the internal "inside-out" perspective, which identifies the organization's impact on society and the environment.

Outcome of the Double Materiality Assessment

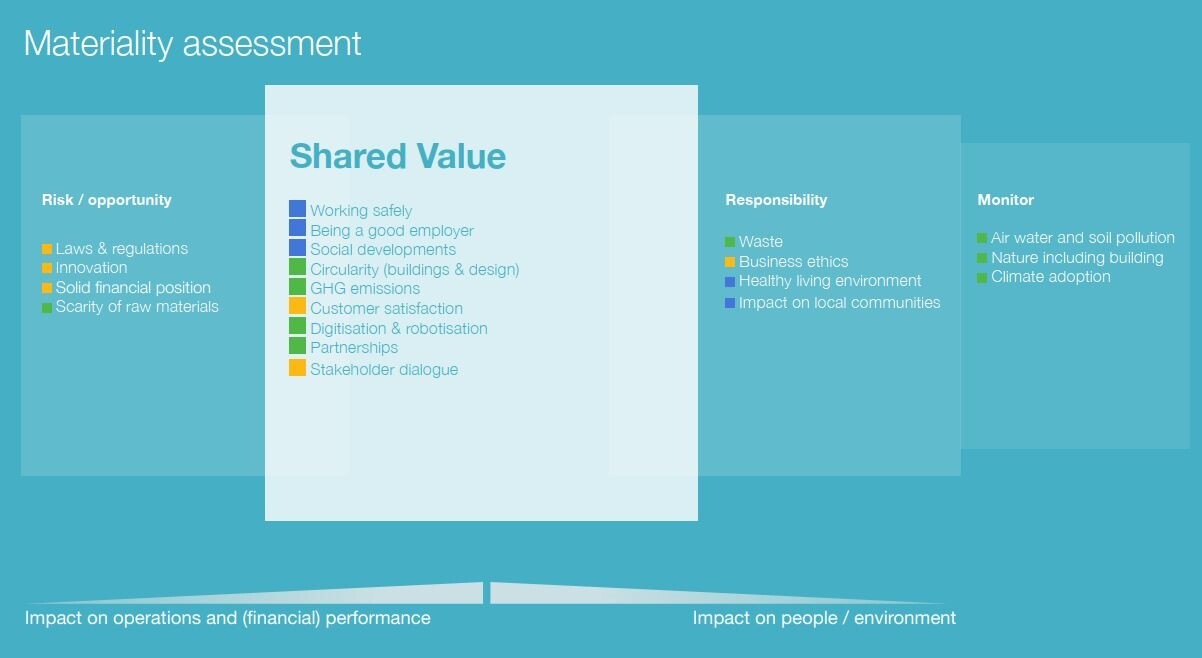

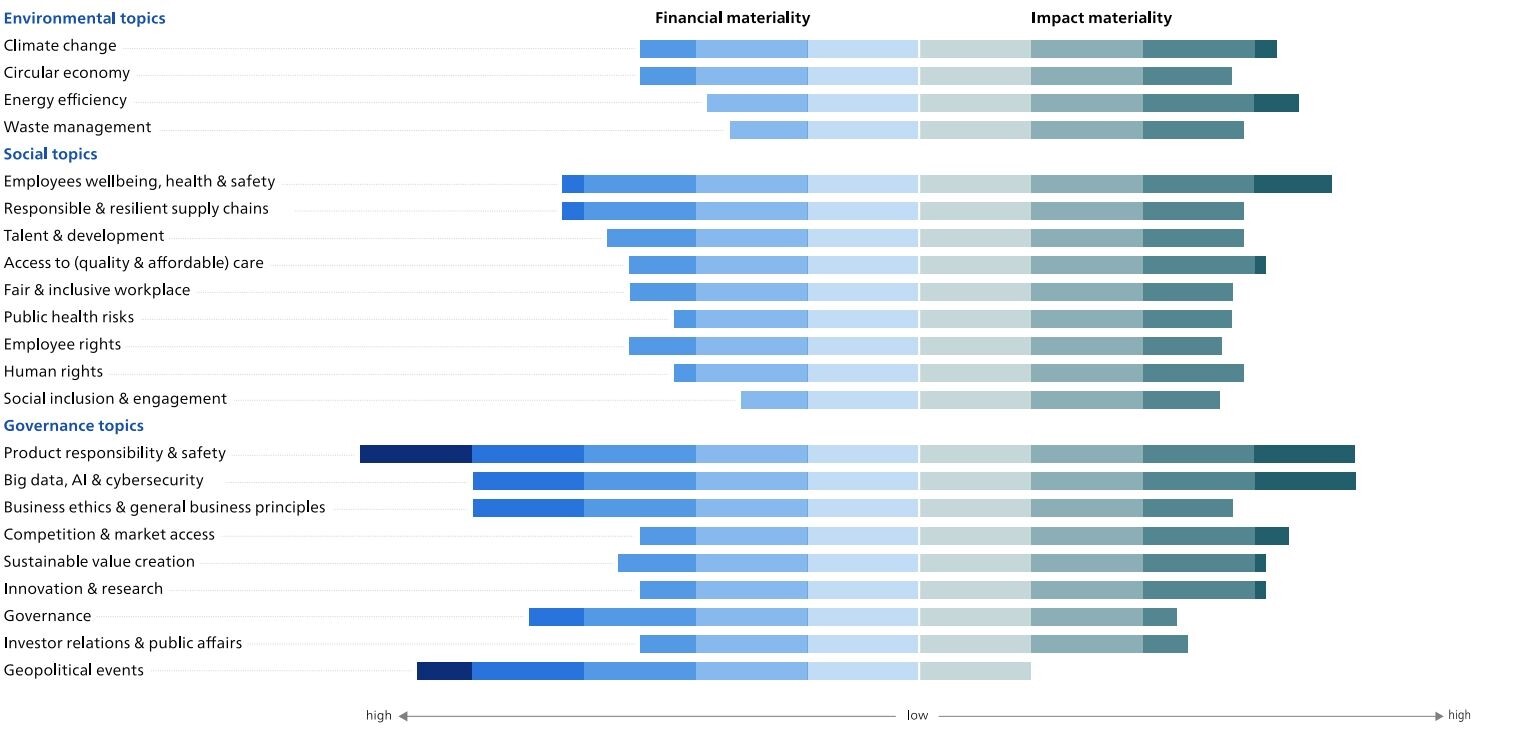

The outcome of the double materiality assessment (please read our article about: HOW TO DO A DOUBLE MATERIALITY ANALYSIS THAT COMPLIES WITH CSRD) is a list of topics prioritized by financial materiality and/or impact materiality. Many companies visualize this through matrices or lists highlighting differences between financial and impact materiality. See below for examples from Daiwa House Modular Europe and Philips.

So What’s Next?

Identifying your company’s critical sustainability topics is just the starting point. These topics, encompassing impacts, risks, and opportunities, should prompt a review of your company strategy to integrate these essential elements comprehensively. With the CSRD laying the groundwork, the European Sustainability Reporting Standards (ESRS) offer detailed guidance on the specific disclosure requirements.

CSRD GAP analysis

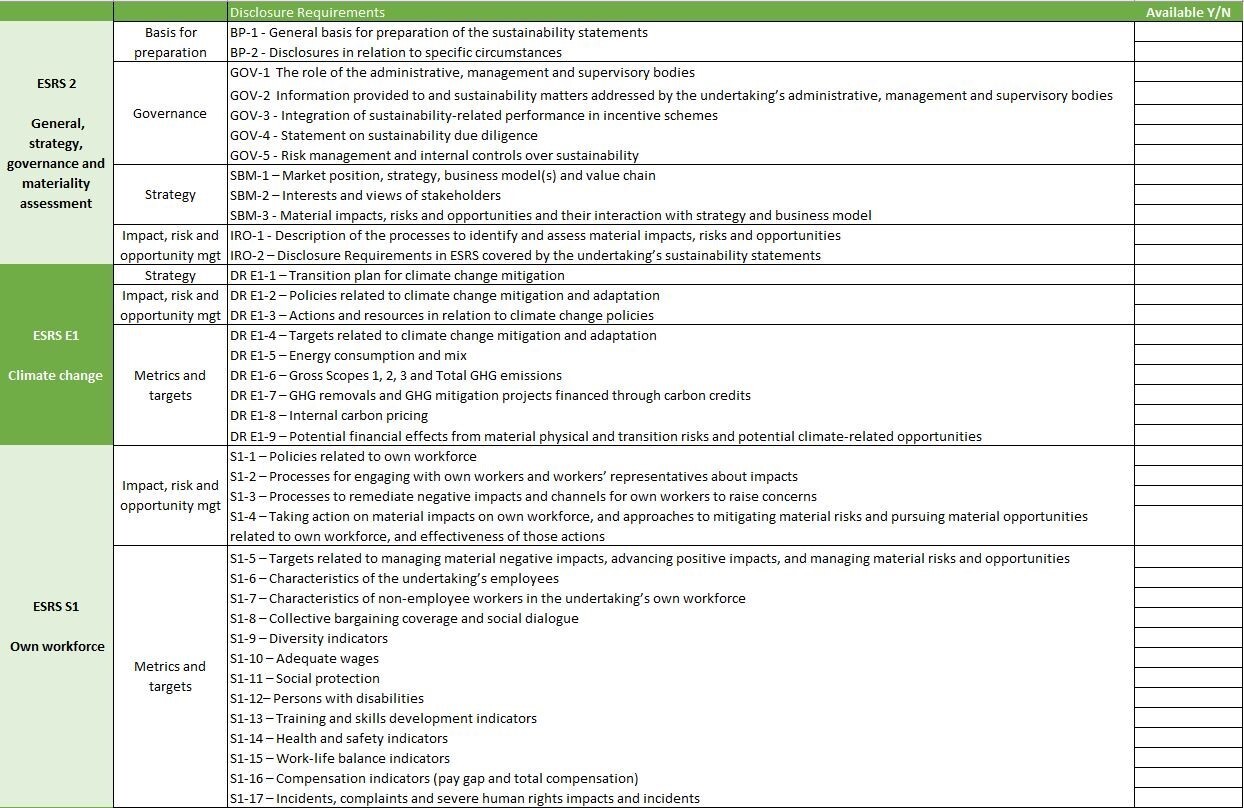

Based on the materiality assessment, you can begin reviewing all relevant disclosure requirements for your company. These requirements specify exactly what needs to be reported. Below is a selection of the 82 disclosure requirements. ESRS 2 applies to all companies, and the remaining requirements depend on the outcome of your double materiality assessment. Overall, ESRS’s require defining policies (P), targets (T), actions (A), and metrics (M) for each material topic. Details are provided in each ESRS.

(picture above: examples of a selection of the 82 Disclosure requirements of 3 ESRS: ESRS2, ESRS E1, ESRS S1)

If you delve deeper into each disclosure requirement, you’ll find detailed overviews and descriptions of what your organization is expected to disclose. ESRS’s differentiate between mandatory (shall) and voluntary (may) disclosures. For all material topics, companies must disclose policies, actions, metrics, and targets. ESRS2 outlines minimum disclosure requirements (MDR), while each ESRS specifies more detailed requirements. In below table you find the minimum disclosure requirements.

| Policies | Actions | Metric | Target |

|

-what is the content of the policy, its objectives, material impacts, risks or opportunities the policy relate to and the process for monitoring; |

-what are key actions taken in the reporting year and planned for the future, their expected outcomes and, how do the actions contribute to the policy objectives and targets; |

-what are the methodologies, assumptions and limitations behind the metric; |

-how does the target relate to the policy objectives; |

Note: there are also phase in criteria’s of up to 3 years for specific section such as the financial resources allocated which are not explained in this section *operational expenditures **capital expenditures

If, for instance, Health & Safety is material for your company, you are required to disclose the company’s Health & Safety policy, the targets you have set, as well as the actions planned to achieve those targets and how progress is measured. Below, you will find additional details about the Health & Safety metrics that a company would need to disclose (DR ESRS S1-14).

| DR S1-14: Health and safety metrics |

| The disclosure required shall include the following information, where applicable broken down between employees and non-employees in the company’s own workforce: -% of people in its own workforce who are covered by the company’s health and safetymanagement system |

| -# of fatalities as a result of work-related injuries and work-related ill health. This information shall also be reported for other workers working on the company’s sites, such as value chain workers if they are working on the company’s sites. |

| -# and rate of recordable work-related accidents; |

| -# of cases of recordable workrelated ill health, subject to legal restrictions on the collection of data (company's employees); |

| -# of days lost to work-related injuries and fatalities from work-related accidents, work-related ill health and fatalities from ill health (company's employees) The company may disclose -the information specified in points (d) and (e) of paragraph with regard to non-employees. -% of its own workers covered by a health & safety management system and if it has been internally audited and/or certified by an external party. |

How TOSCA can help

Navigating a Gap Analysis to ensure your report aligns with CSRD can be daunting, but TOSCA is here to assist. Our comprehensive CSRD Gap Analysis service includes review sessions with subject matter experts tailored to your material topics. We evaluate all available information, align them against the ESRS with our intuitive tools, identify any discrepancies, and collaboratively develop a roadmap to address these gaps, ensuring your organization's CSRD compliance.

Get more information on the CSRD GAP analysis - without obligation

Reach out to Ulrike ulrike@toscatribe.nl or call +31(0)6-51072464.

Back to news